Be YOUR OWN Credit Master by following these simple hints

Your credit score is also referred to as a FICO Score and is a mathematical formulae created by Fair Isaac and Company. The credit score is used by most companies to see if you are a good credit risk or not. Equifax and Trans Union will crunch the numbers from the credit report, and spit out a number somewhere between 300 and 900, or even no number or R for Reject.

Even though more than 50% of the population have a credit score of over 750, from a lender’s prospective, a score over 680+ is considered excellent. A score of over 620 is considered good. Below 620 and creditors become selective on the amount of credit they will extend and of course the interest rate they will charge.

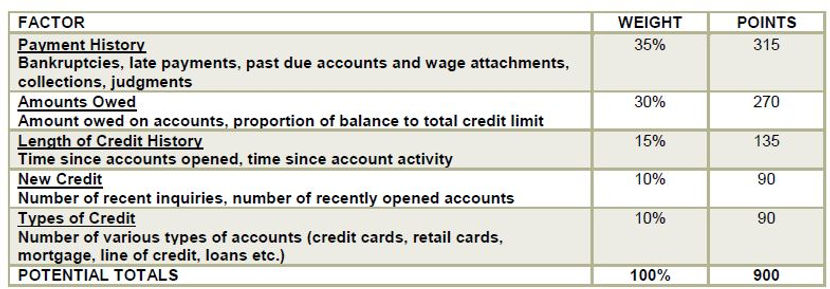

Scores are calculated based on five key areas. Here is a chart for your reference and below that we have highlighted the areas that we need to address based on your current credit bureau;

Below is a simple explanation on what each items means and how you could leverage each single one to start improving your credit, yourself!

-

Payment History: measures payment history on such items as bankruptcies, late payments, past due accounts, and wage attachments, collections, judgments and etc. Three factors will determine the size of the deduction in score:

-

Time passed since the payment blip

-

Number of missed payments

-

How bad the blunder was

-

-

Amounts owed:

-

Keeping the balances outstanding to less than 75% of the available credit limit will INCREASE the score.

-

Balances above 75% of the available limit will DECREASE the score

-

Installment loans and maxed out Lines of Credit immediately reduce the score on approval but then slowing increase score when under 75% of limit.

-

-

Length of Credit history:

-

Favorable weight going to those who have had credit for the longest time

-

Past credit behavior is a good indication of future behavior. This establishes a foreseeable pattern of behavior.

-

-

New Credit:

-

This is measured by the number of “hard” credit enquires

-

Acceptable limits: Less than 4 to 6 enquires in the last 12 months is within acceptable limit.

-

Unacceptable Limit: More than 6 enquires in the last 12 months are above an acceptable number and will impact the score negatively.

-

Do NOT allow anyone to pull a credit bureau on you unless it is absolutely critical

-

-

Types of Credit: In contrary to the general public opinion, the more credit you have, the less your debt ratio would be and it will positively help your credit score. Also, having different types of credits (credit cards, line of credits, mortgages) will improve tour score as well.

We hope these simple hints could help your personal finances and increase your understanding on how credit works. Needless to say, we did not want to burden the topic with complex mathematical formulas and credit models. After all, this is our job!

In Kam real estate solutions Inc, before we approve you for your Rent To Own program, we would do an extensive financial and credit analysis on your specific case. Although it might take some time, this will maximize your success rate in our Rent To Own program and will ensure that you will have a clear and successful path ahead to finish the program.

If you are interested in our Rent To Own Program, click HERE, and get in touch! We would be happy to help you out in your home ownership journey.